Dear Aspirants, LIC HFL is one of the most important exam in the competitive examination. LIC HFL mains exam consists of three sections i.e. Reasoning ability and Numerical Ability, General knowledge & Current affairs and Insurance & Financial Market Awareness. LIC HFL Insurance Awareness & Financial Market Awareness section comprises of 50 questions. LIC HFL Insurance Awareness Questions 2019 play an important role in boosting up the score in mains examination and also helps in the interview. Here we are providing a new series of LIC HFL Insurance Awareness Questions 2019. Aspirants can make use of this LIC HFL Insurance Awareness Questions 2019, to improve score in the Insurance & Financial Market Awareness section.

Check Here for LIC HFL Mock Test Series 2019

Click Here to Subscribe Crack High Level Puzzles & Seating Arrangement Questions PDF 2019 Plan

[WpProQuiz 7178]1) In Insurance, CGL stands for?

a) Commercial General Liability

b) Common General Liability

c) Captive General Liability

d) Control General Liability

e) None of these

2) ________ is an insurance coverage protecting the manufacturer, distributor, seller of a product against legal liability resulting from a defective condition causing personal injury, or damage, to any individual or entity, associated with the use of the product.

a) Product Liability

b) Unauthorized Reinsurance

c) Retro cession

d) Retrospective Rating

e) None of these

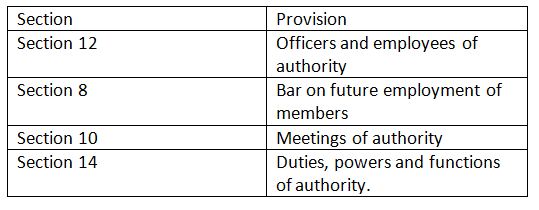

3) Which Section of the IRDA Act 1999, specifies the duties, powers and functions of the authority?

a) Section 12

b) Section 8

c) Section 10

d) Section 14

e) None of these

4) The Insurance Advisory Committee advises IRDAI on development, disclosures and regulatory aspects of the insurance industry. The Committee cannot have more than ________ members at any point of time.

a) 15

b) 20

c) 25

d) 10

e) None of these

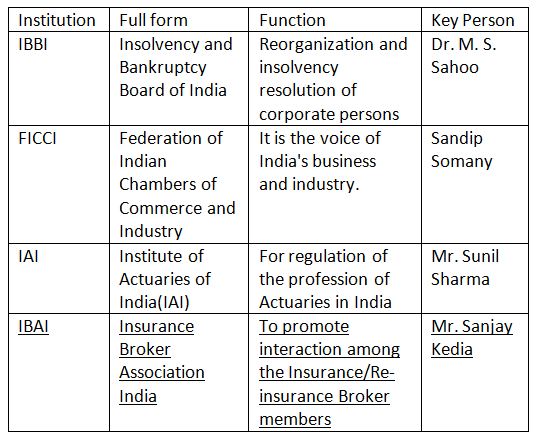

5) Which among the following is an IRDAI recognized apex body of licensed Insurance Brokers?

a) IBBI

b) FICCI

c) IAI

d) IBAI

e) None of these

6) In case of an individual, the proposed shareholding in the paid up equity capital of the insurance company is capped at ________ percent.

a) 10%

b) 5%

c) 20%

d) 12%

e) None of these

7) The first ever life insurance industry in India was set up in which city?

a) Bombay

b) Delhi

c) Madras

d) Calcutta

e) None of these

8) Since which year, IRDA started licensing private sector companies to conduct general insurance business in India?

a) 1999

b) 2001

c) 2004

d) 1992

e) None of these

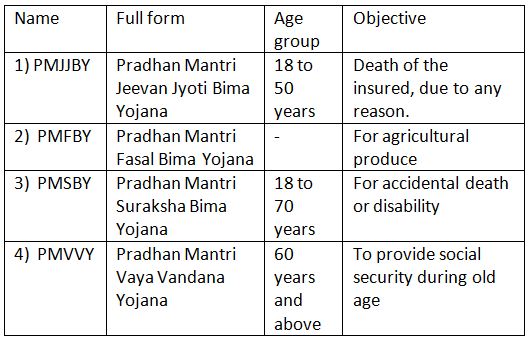

9) Which among the following is an accidental insurance scheme?

a) PMJJBY

b) PMFBY

c) PMSBY

d) PMVVY

e) None of these

10) What does ‘Paid Up’ policy mean in insurance?

a) Policy that requires no further premium payments and continues to provide benefits till maturity.

b) Policy that provides a life cover for a specific term

c) Policy for which the premium is paid in a single period together

d) Policy in which the premium gets reduced over a period of time and benefit increases till maturity

e) None of these

Answers :

1) Answer: a)

In Insurance, CGL stands for Commercial General Liability. General liability coverage for organizations is provided under the Commercial General Liability Policy (CGL).

The CGL is designed to ensure those general liability exposures that are common to most organizations, premises and operations, products and completed operations, liability arising out of independent contractors, and contractual assumptions of liability.

2) Answer: a)

Product Liability is an insurance coverage protecting the manufacturer, distributor, seller of a product against legal liability resulting from a defective condition causing personal injury, or damage, to any individual or entity, associated with the use of the product.

Retrocession: The amount of risk that a reinsurance company reinsures or the amount of cession that the reinsurer passes on.

Retrospective Rating: The process of determining the cost of an insurance policy after the expiration of the policy, based on the loss experience under the policy while it was in force.

3) Answer: d)

The Section 14 of Chapter IV of Insurance Regulatory and Development Authority Of India Act, 1999 specifies the duties, powers and functions of the authority. Additional information about other sections is provided in the following table:

4) Answer: c)

The Insurance Regulatory and Development Authority of India released a notification on 21st March, 2017 for the Reconstitution Insurance Advisory Committee. The decision was taken according to sub section (1) of Section 25 of the IRDA Act, 1999. Total members of the Insurance Advisory Committee are 25.

5) Answer: d)

IBAI is an IRDAI recognized apex body of licensed Insurance Brokers. Additional information about other institutions is given in the following table:

6) Answer: a)

In case of an individual, the proposed shareholding in the paid-up equity capital of the insurance company is capped at ten (10) per cent. Paid-up capital is defined as the amount of money a company has received from shareholders in exchange for shares of stock. IRDAI (Transfer of Equity Shares of Insurance Companies) Regulations, 2015 mentions the provisions related to paid-up equity capital of the insurance company.

7) Answer: d)

The first life insurance company on Indian Soil was the Oriental Life Insurance Company, started by Europeans in Calcutta in the year 1818.In 1870, the Bombay Mutual Life Assurance Society started its operations as the first Indian life insurance company.

8) Answer: b)

Since 2001, IRDA started licensing private sector companies to conduct general insurance business in India.The IRDA opened up the market in August 2000 with the invitation for application for registrations. Foreign companies were allowed ownership of up to 26%.

The Insurance Regulatory and Development Authority (IRDA) was constituted in 1999 as an autonomous body to regulate and develop the insurance industry according to the recommendations of the Malhotra Committee.

Chairman, IRDAI : Dr. Subhash C. Khuntia

9) Answer: c)

Pradhan Mantri Suraksha Bima Yojana (PMSBY) provides accidental insurance coverage. Information about other insurance schemes is given in the following table:

10) Answer: a)

Paid-up Insurance Policy: An insurance policy that requires no further premium payments but continues to provide coverage.

Participating Policy: A type of insurance policy that allows policy owners to receive policy dividends. Also known as par policy.

Package Policy: A single insurance policy that combines several coverages previously sold separately.

Leave a Reply